Market Updates

Predictions update for July, 2022.

An update on the markets for summer 2022. Plus, a few predictions from my last post on this – these are not all mine but common ones that have been making the rounds since 2020. This post is mainly of my #4 prediction from last year on the stock and real estate correction.

In addition to the stock and real estate market, there was the use of lockdowns for climate issues, mixing the same ‘emergency’ messaging as was done with COVID lockdowns.

This didn’t have a massive roll-out, but some regions did use this messaging on small populations, such as in France, where officials decided on limitations of movement and gatherings due to hot weather. Hot weather that is or was no way record-breaking, but now subject to the government looking after your safety for you, rather than you doing something racist and selfish, like using common sense. Again, not a massive control of huge areas, small and targeted, but enough to start planting the seeds of doubt in people’s minds. Same way that nowadays, any small heat wave is a ‘deadly heat dome’, not just a normal few days of heat.

(For a summary of these events from last week, James Corbett and James Pilato have their usual good run down of the new normal events for third week of June here).

Other predictions in that list are still ongoing – rising inflation, continued disruptions on food supplies, and the continued erosion of the Western ‘democracies’. The pandemic narrative (for any virus) remains ‘soaking’ in the background as usual.

I have been watching the markets more over the past year, noting the huge run-ups in all sorts of equities and industries. A 20-30% correction was in my list of predictions from last year (which is easy to say since the markets always correct at some point). Many of the tech stock ‘crashes’ like Tesla, Apple, Amazon, etc. simply only dropped their share price back to the high levels of late 2020/2021. The ‘crash’ now is mainly among the value-stocks and ETFs, like financials, materials, some commodities. But even those ‘pullbacks’ are simply erasing the 20-25% run-up that took place early 2022. They are just returning to the already-high levels of the 2021 run-up. It seems to me like there is still room for more psychological ‘scares’ or nudges, combined on both the real-estate side and stock market. For most of the middle class these are so intertwined since people sell off portions of both when things get jittery. The fearful masses as usually look to the ‘news’ for how to think, and how to act, and so when the experts and talking heads go on the MSM, they can literally tell people how to be scared, and what measures to follow to ‘stay safe and do your part for <insert scary event here>’.

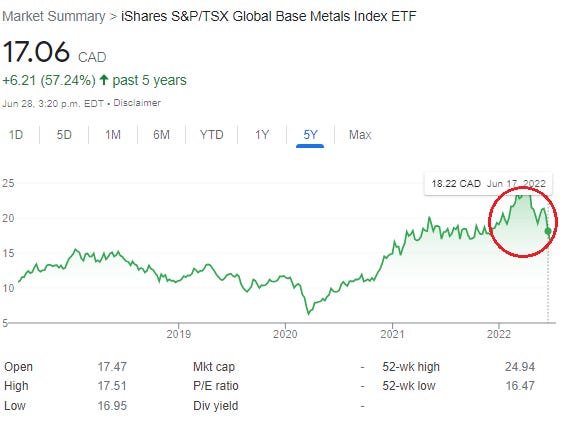

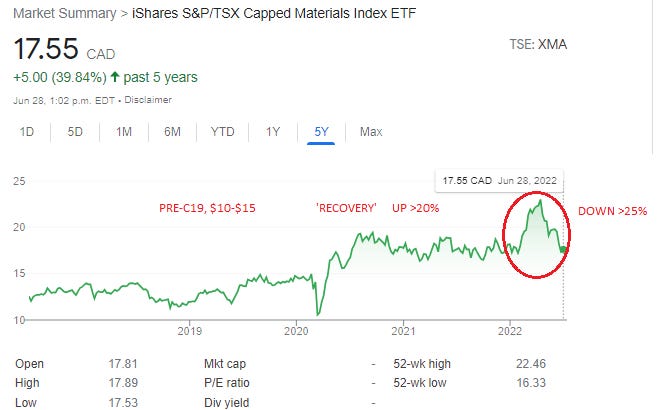

Below are just a couple of the broad-based ETF categories reflecting the price drops recently. I choose Blackrock iShares of course since they either already own/control a huge portion of these sectors and will consolidate even more ownership/control in the coming years. Those companies who do not tow the line for the global ESG-based investments will be pushed in to compliance or simply excluded from the market. When they say you’ll own nothing, they are telling the managerial classes and their fund managers that they are the only way to profit off the Earth and its resources, so get in line.

Both the above charts for basic material and metals show that the recent ‘crash’ has only returned us to the 2021 high levels. There is still room for further drops, at which point I’m sure the institutions will buy-back at the lower levels, sealing the losses for the retail buyers who’ve been buying in during 2022, chasing the gains.

One difficult part of this is that the feds in most countries are manipulating their own bond markets and even silver and gold markets, so it’s difficult to look at the normal signs and correlations, such as the US 10-year T-bill yield and others. The Shiller price-to-earnings tracker for the broad S&P500 indicates this latest ‘crash’, like the two Blackrock ETFs above, has only returned us to the previous elevated high of early 2022. The PE ratio spiked to 37 in Spring 2022 and is now back to about 30. Before the 2008 “Great Financial Crisis” (of our lifetime etc. etc.), this same tracker peaked out at 27. At that point, indices such as inflation (‘official’) and bond yields were close to 4-5%. As we hit a PE ratio of >30, the interest rates were below 2 or 3% (rising now of course).

The US 10yr treasury yield has also been building in the rate hikes prior to each announcement, along with a corresponding drop in the stock market. We are approaching levels of the pre-2008 GFC, where the reply there was to drop the interest rate immediately after the crash. Could we be seeing the same pattern here? Sharp run-up in rates, crash, then rate hike reversals to ‘save the system’?

And the Blackrock high-yield corporate bond fund has also fallen back to levels of the GFC in 2008-2009, dropping more than 15% in the last year (2021 to 2022).

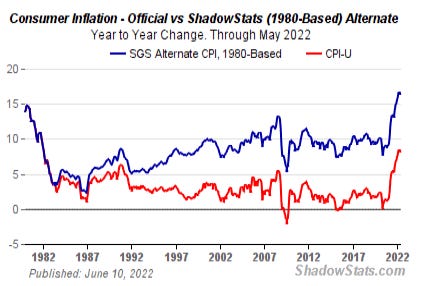

The big ‘trigger’ could still be the true inflation rate. Back in 2008, the official government rate was reported as close to 5% - yet using the shadowstats method (keeps more energy/food in the CPI basket), the true rate was closer to 13%. Compared to today’s rates, we are now close to 8% ‘official’ and 17% actual:

Chart Courtesy of shadowstats.com

As mentioned before, inflation is a policy tool used by government. Inflation is always portrayed as a tough economic struggle that our dutiful politicians try to fight for the good of the people. Typically, its narrative is always ‘we really have to balance unemployment against inflation’, or some other metric that the public is always fearful of. ‘Great Inflation’ events have always been exploited in the past to provide short, sharp cultural shifts in (mainly) Western societies. So, I feel this next reset will be similar, but in proportionally-larger scale similar to the levels of inflation today versus 2008. You can just see the tail-end of the previous cultural shift of the 1970s in the shadowstats chart, near 1980 at 15%. Since they used the same mixes of energy and food CPI back in 1980, the ‘official’ and actual inflation rates matched. The interest rate at that peak was 18% or so. I think these days just hinting at anything more than 7 or 8% is enough to trigger their ‘black swan’ to pop this ‘everything-bubble’.

The high inflation versus ‘official’ is also needed by governments. It’s the easiest way to pass debt on to the masses and earn a yield (the real yield for bonds is still negative after inflation), while directing the public anger at scapegoats in the MSM. Right now, it’s evil Putin bad, soon to most likely be joined by evil China threatening Taiwan, which will provide many more months of supply chain ‘shocks’ that can be used to keep inflation high.

I feel there’s still a few more weeks or months to scare the public via ‘surprise’ rate hikes. They could even ‘admit’ that they were wrong, that they didn’t see the true >7% inflation (as Yellen did recently), and have to aggressively hike the rates to match to ‘fight inflation’. They would still be passing debt on to the public since the true rate is >15%. It comes down to the ‘soft landing’ versus ‘total collapse’ opinions of outcome. I still feel it will be deeper and sharper than 2008-2009 for both real estate and stocks. But the true ‘collapse’ event, which will supply the shock to accept CBDC, is off in 2025 or later while they work in the background on other goals.

And to end the doom-and-gloom with a little bit more black-pill/white-pill discussion, I recommend Jerm Warfare’s latest interview and update with Iain Davis (“Pseudopandemic”). Provides a great update to the shift of power centre from the West to the East, including the effects on the huge oil and gas markets worldwide. Not that the East (BRICS or Russia/China) are the enemy of the West who are not following the WEF narrative. They are parroting the same goals and agendas with only slightly different language – the transfer being pushing down the middle-class wealth of the West to prop up the elites of the East. The common enemy of all blocks remain the citizens.

Iain Davis: “The hard thing people still cannot get their heads around…People still cling to this idea that some government person is going to save them. They’re not, they’re just puppets for people who don’t care about us, and we are just their consumers”.